Stay in School?

Everyone starts school with the intention to graduate. But sometimes life gets in the way and it can be hard to stay the course.

It’s normal to face some road blocks on your way to getting your degree, and you may even need to take longer than anticipated to reach the finish line. It doesn’t matter how you get there – but getting to that degree may be one of the smartest financial moves you can make!

When choosing whether or not to stay in school, consider the following:

- Dropping out before the end of the term means you may not have “earned” the federal aid you received. You may need to repay those funds to the school immediately, and cannot reenroll until you do.

- Students who leave school are more likely to default on student loans1:

- 49% default rate for dropouts

- 10% default rate for those who attained bachelor’s degree

- Degree holders have greater annual salaries2:

- High school diploma only: $35,615

- Bachelor’s degree: $65,482

- Advanced degree: $92,525

- This translates to greater lifetime earnings3:

- High school diploma only: $600,000

- Bachelor’s degree: $1.2 million

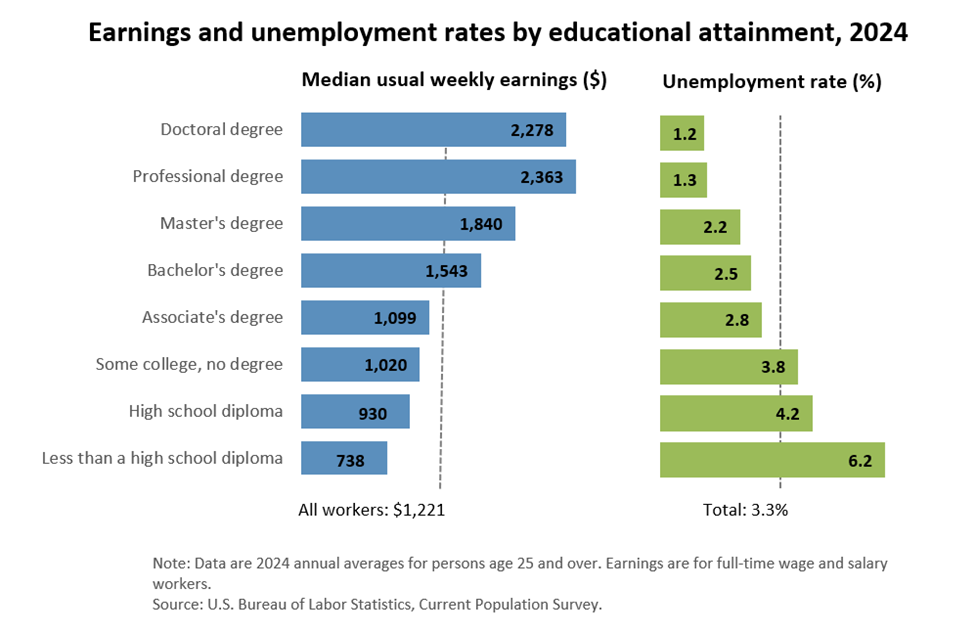

- Unemployment rates for degree holders are lower4:

- More and more jobs are requiring a degree:

- Only 34% of American jobs require a high school diploma or less5

- 99% of job growth between 2010 and 2016 went to workers with associate’s, bachelor’s, or graduate degrees6

- By 2020, 65% of all jobs will require some postsecondary education7

1 National Center for Education Statistics, “Datalab, Beginning Postsecondary Students 2004-2009, Table cdmbhm7a.

2 https://www.census.gov/newsroom/press-releases/2017/cb17-51.html

3 http://www.hamiltonproject.org/charts/lifetime_earnings_by_degree_type

4 https://www.bls.gov/emp/ep_chart_001.htm

5 https://cew.georgetown.edu/wp-content/uploads/trillion-dollar-infrastructure.pdf

6 https://cew.georgetown.edu/wp-content/uploads/Americas-Divided-Recovery-web.pdf

7 https://cew.georgetown.edu/wp-content/uploads/2014/11/Recovery2020.ES_.Web_.pdf